“Pay yourself first.”

I don’t recall when it was that I first heard – or perhaps read – that simple bit of financial wisdom. But I do know it was sometime way back in my younger days, and that it sure sounded right – like something that I really ought to try to do.

There was no Google back then, but if you enter the phrase “Pay yourself first” in your favorite search engine today, you’ll learn that it means exactly that. Those who adopt this practice are sure to set aside some amount of money – no matter how small, but as much as they can – from each and every paycheck in order to save it for themselves.

In my case (and to put a twist on an old cliché), this means I should pay Paul before paying Peter – who, in this case, represents all the other bills I need to pay and financial obligations I need to meet.

Back in 1982, when I began my federal career, paying myself first wasn’t as easy as it is now. It involved setting up some sort of investment account on my own and probably paying some fairly high fees.

But then, five years into my career, paying myself first became a lot easier and a lot cheaper. That’s when federal employees like me were first allowed to begin investing part of their paychecks into something called the Thrift Savings Plan.

The roots of the Thrift Saving Plan can be traced back to the late 1970s, when a change in the Internal Revenue Code – as outlined in Section 401(k) – allowed individuals to avoid paying federal taxes on deferred compensation, within defined limits. This enabled everyday Americans to set up their own little tax shelters, where they could place untaxed money that wouldn’t be subject to taxation until they withdrew it, provided they didn’t withdraw it too soon.

401(k) plans exploded in popularity when the IRS allowed payments into these plans through payroll deduction, and when private companies began matching some of the payments made by employees. This was accompanied by the demise of traditional pension plans, shifting much of the burden for retirement savings to individuals.

The nation’s largest employer, sometime affectionately referred to as Good Ol’ Uncle Sam, got in on the act in 1986, when Congress passed legislation reforming the retirement system for federal employees.

The law set up a system that’s been compared to a three-legged stool, because it consists of three components – Social Security, a relatively small pension, and the Thrift Savings Plan, a tax-sheltered investment vehicle similar to 401(k) plans in the private sector.

This triad was dubbed the Federal Employees Retirement System – inevitably shortened to FERS – and it covered all federal employees hired after New Year’s Day in 1984.

Because I came on board about 18 months prior to that date, I was grandfathered into the old Civil Service Retirement System, also known as CSRS and sometimes called “scissors.” You could say that I made the cut, though I did have the chance to transfer into FERS during subsequent open seasons.

In the end, I stuck with CSRS, meaning that I pay into a separate annuity system rather than Social Security. This puts me into a small and diminishing group, consisting of the approximately 4% of active federal employees who are still covered by CSRS.

As a CSRS employee, though, I could still put money into the Thrift Savings Plan through payroll deduction. So that’s exactly what I did, pretty much as soon as I could.

Unlike my coworkers covered by FERS, I did not get, and still do not get, matching government contributions into my individual TSP account. If you are covered by FERS, those contributions range up to 5% of your basic pay, depending on how much you put in. This means that you double your money as soon as you invest it, and it’s hard to beat that.

Even without a matching contribution, though, opening a Thrift Savings Plan account offered many advantages. For one, the administrative fees are microscopic, amounting to less than one-tenth of 1% your total investment. Depending on the TSP fund, those fees are now between 50 and 60 cents per $1,000 invested, well below what any private fund or broker would charge.

Add to that the convenience of automatic payroll deduction, which meant that paying myself first was easy and relatively painless and that I could give myself a raise when financial circumstances allowed. Finally, the portion of pay I put into my TSP account is exempt from federal taxes, which lessens the impact of TSP payments on my take-home pay.

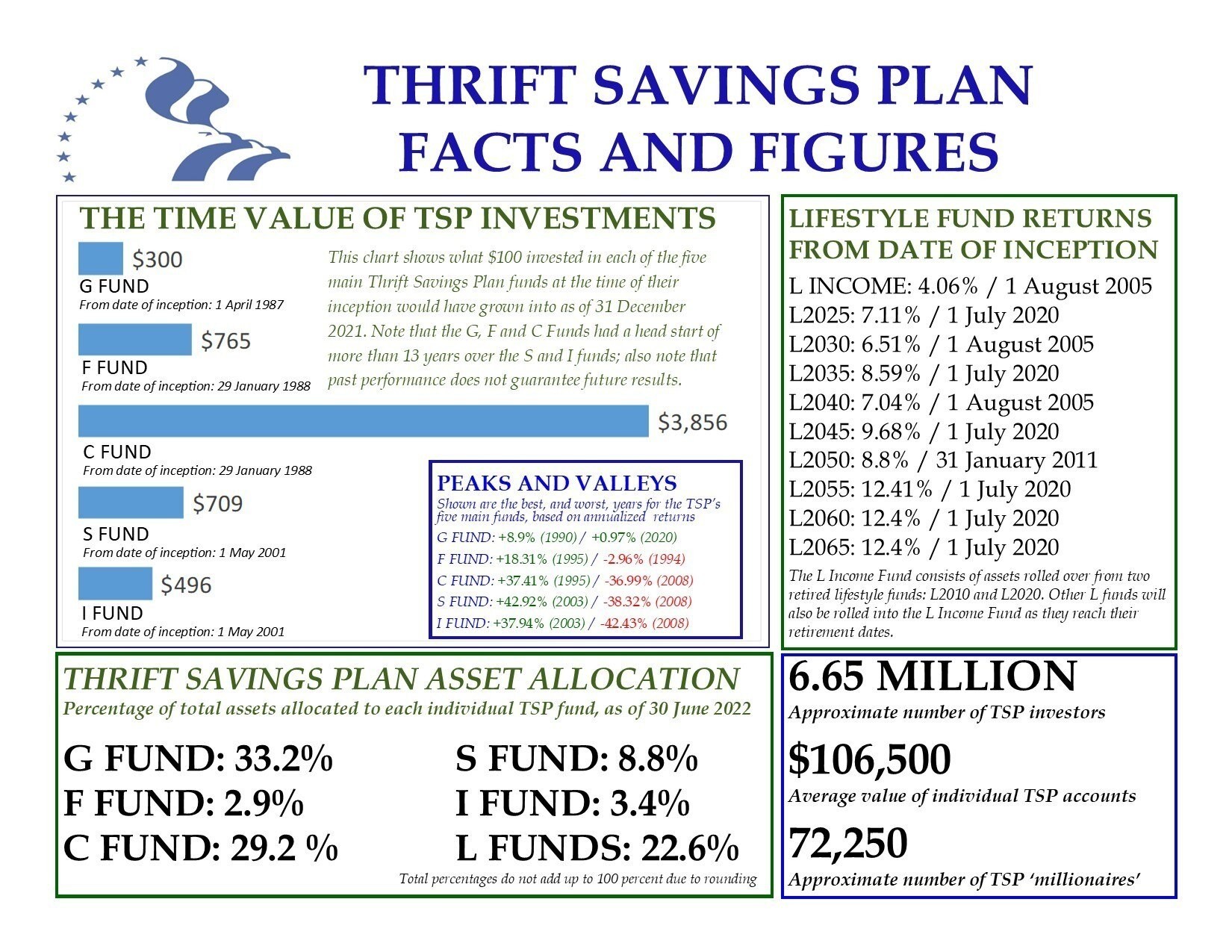

When the Thrift Savings Plan was first opened to investors in 1987, the only option was the G Fund, made up of short-term U.S. Treasury securities backed by the full faith and credit of the federal government. The G Fund has never lost money, making it a “safe harbor,” but its interest rates tend to be relatively low.

One year later, two other funds were open to TSP investors: The F Fund, made up of fixed-income bonds, and the C Fund, made up of common stocks. These funds can, and indeed do, sometimes lose money, but also can and have posted impressive gains, depending on the market’s overall performance.

In 2001, the S Fund – made up of small-capitalization stocks – and the I Fund – made up of international stocks – were added to the Thrift Savings Plan. These funds are high in risk, but potentially high in returns, as their performance over the past two decades has shown.

Today, TSP investors can also put their money into 10 different L Funds. Short for Lifecycle, these funds use algorithms to determine what mix of investments is right for an individual based on their projected retirement date.

If you’re young and starting out, the L Fund designed for you would be largely made up of common stocks and other securities that offer higher risk but also potentially higher returns over time. If you’re fast approaching retirement (like me), the L Fund you choose should consist of investments that are lower in risk but may offer lower returns in the short run.

Ten years ago, the Thrift Savings Plan began offering a Roth option. Contributions to a Roth TSP fund are made with post-tax money (versus pre-tax for traditional TSP funds) but are generally tax-free when withdrawn. Note that the money you placed in traditional TSP funds will be taxed when it is withdrawn, so adding a Roth option could lower your tax liability in retirement.

Yet another option was added to the Thrift Savings Plan earlier this year when more than 5,000 different mutual funds were opened to TSP investors. Be aware that, if you choose this option, you must pay some substantial fees, in comparison to the very low fees charged for the traditional, broad-based TSP funds. In addition, you must have at least $40,000 in your TSP account before you can begin investing in mutual funds under the plan.

The number of investment options offered through the Thrift Savings Plan allows TSP investors to tailor their accounts according to their individual needs and goals. However, it can also sow confusion, because how do you really know what’s right for you?

Well, since it’s impossible to know with 100% certainty what the future holds, it’s impossible for any of us to make perfect TSP investments that bring the highest possible return. Then again, if you knew how to time the market (and nobody really does), you wouldn’t need to be working here.

Looking back, there are times when I could have made better decisions regarding my own TSP account. But while I was far from perfect, I have seen my account grow into a nice nest egg that I’ll be able to draw on in my fast- approaching sunset years.

In the end, what really matters are your financial goals and your timeline. Always keep in mind that the Thrift Savings Plan isn’t a “get rich quick” scheme. It’s designed to help you save for your retirement.

Let’s say you have a few decades to go until retirement and the C Fund portion of your TSP account declines in value (as it surely has this year). Oh no, you’ve lost money!

Actually, you didn’t. In fact, you should look at this as a buying opportunity. When the market declines, the same amount of money going into your TSP account will buy more shares. When the market rebounds, as it historically always has, those shares will rise in value and your TSP account will grow even larger.

In other words, you’re buying low and selling high. Isn’t that what we’re supposed to do?

But don’t take my word for it. Look at the charts accompanying this article. Better yet, go to the official Thrift Savings Plan website, www.tsp.gov.

There’s a wealth of information there, on historic Thrift Savings Plan returns and anything else related to TSP. You can even sign up for informative webinars on a variety of topics. I recently took some of these webinars myself on topics relevant to my own situation, including making withdrawals from TSP and (gulp!) TSP death benefits.

Look, I get it. The cost of everything has gone up lately, and we all have bills to pay and other financial obligations to meet, like saving for college for your kids or paying off your own student loans.

As I can attest, though, it will be to your long-term advantage to make room in your budget to put part of your pay into the Thrift Savings Plan. Remember where we started: “Pay yourself first.”

After all, who deserves it more?

Social Sharing