FORT KNOX, Ky. — There is no time like the present to review personal financial report cards and learn the importance of understanding credit.

By making informed financial decisions, avoiding costly mistakes and preserving financial stability, individuals can improve and secure a better financial future. Afterall, understanding and managing credit effectively is the key to financial success.

One’s credit score is more than just a number, it defines a consumer’s financial reputation and determines if the person is responsible enough in money management skills to reap the benefits that lenders offer, such as qualifying for better insurance rates, securing a loan and qualifying for rental options and job opportunities. Credit ratings determine creditworthiness, which establishes how much lenders offer and the premiums they charge.

According to the Consumer Financial Protection Bureau, numerous credit changes are being implemented in 2025.

Forbes estimated the changes could benefit 15 million Americans: “Lenders are tightening approval standards. Some will see higher credit scores, while others will find it harder to get approved for credit.”

Here’s what is new in the world of credit:

- Artificial Intelligence (AI) and alternative data are reshaping how credit is scored; new credit scoring standards are being implemented.

- Lenders are transitioning to alternative data scoring models to reduce defaults, minimize fraud, and improve the ability to borrow with success. Artem LaLaiants of RiskSeal said, “By using ‘digital footprints,’ financial institutions can interact with various platforms to enhance the underwriting process more accurately, predict who is considered high risk, and determine various character traits and risky behavior that indicates a tendency toward default.”

- LaLaiants continued: “This precision will identify red flags – considered signs of instability and probability of default – and combat fraud by improving the quality of a credit portfolio, thus, increasing the number of approved loans, and impacting approval rates, revealing reliable financial behaviors of those who might otherwise be deemed as high-risk.”

- Changes impacting credit scores:

- New credit will increase the “amount owed” in credit utilization (how much credit is being used compared to the total credit limit), potentially lowering a consumer’s score.

- Requesting a credit report will not affect a potential borrower’s FICO scores if it is ordered directly from a credit reporting agency or organization authorized to provide credit reports to consumers, such as the myFICO report.

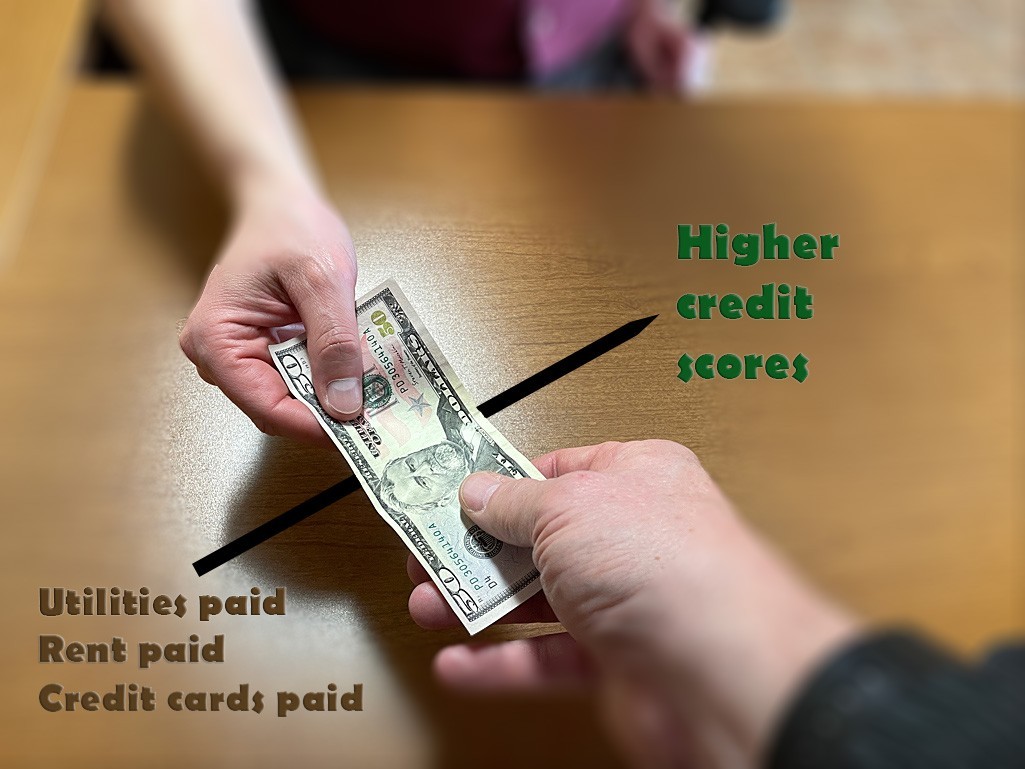

- Vantage Score 4.0, a scoring system developed by the three major credit reporting agencies that includes data which looks at credit usage, is scoring 33 million more people than traditional models. It will now consider an applicant’s payment history for rent, utilities and telecom payments if the applicant has limited loan and credit experience to generate a good credit score. Data for a 6-to-24-month history would determine a more comprehensive view of creditworthiness.

- Some future inquiries will be ignored depending on who is pulling the report. Credit inquiries are a review of a consumer’s credit file made by potential lenders, employers or landlords to assess creditworthiness.

- Utilizing a credit mix – the types of accounts that make up credit, such as credit cards, retail credit, car, student and personal loans, and mortgages – will help diversify the scoring model and prove to lenders that bills can be paid on time.

- Credit bureaus will offer faster updates, correcting inaccuracies on credit reports, which cost consumers more money due to higher interest rates or loan denials. The existing timeline is 30 days to investigate a claim and provide a written resolution if the claim is validated.

- Credit monitoring will become free to help track a borrower’s financial standing and identify opportunities to improve credit.

- The Federal Housing Finance Agency (FHFA) has confirmed that mortgage lenders will cease pulling tri-merge reports from the three major credit reporting agencies (Trans Union, Experian and Equifax), and will instead switch to a bi-merge report.

- Job stability and spending habits will play a role in the credit scoring system where lenders will now analyze behavior through digital transition data: the process of moving old data to a digital format, called “software migration.” This might include new software, cloud computing and AI.

- According to Forbes, borrowers who remain in default on their federal student loans will be hit with negative credit reporting in the coming months, as federal protections that have been in place for nearly five years are expiring. Those who have demonstrated responsible financial behavior will reap the rewards, such as qualifying for lower loan rates, gaining access to higher quality financial products, higher credit limits, a likelihood of housing approval and or housing options, better insurance rates and the possibility to avoid utility deposits when buying or renting.

- Credit repair organizations will be targets. The Ending Scam Credit Repair Act (ESCRA) will crack down on fraudulent practices in the credit world, meaning consumers cannot be billed until at least six months after they have been successful in improving their credit scores with penalties for violations.

- Following are some suggested recommendations:

- Check the three major credit reporting agencies to ensure Credit Bureau Report changes have been made.

- Practice positive credit management by building and maintaining a good credit history, ensuring financial obligations are met without default, performing regular credit checks, liquidating debt, disputing negative information, utilizing credit builder options through your financial institution and keeping credit balances low.

- Always make payments on time. Using AI-drive scoring may help because every on-time payment counts towards a better score.

- Maintain a low credit utilization ratio.

- Avoid unnecessary credit applications.

- Dispute errors listed on your credit report.

- Pull your credit report at least annually to make sure rent and utilities payments are reported to the credit bureaus. Remember, they help build your credit history and give your credit score a boost.

- Utilize financial tools and education, such as the Office of Financial Readiness (FINRA), Army Family Web Portal – OLMS, Consumer Financial Protection Bureau, Military OneSource, Investor.gov, Financial Literacy Education Commission and Thrift Savings Plan

- Define your key objective. Are you applying for a mortgage, purchasing a vehicle or applying for a personal loan?

Benjamin Franklin once said, “Change is the only constant in life. One’s ability to adapt to those changes will determine your success in life.” By keeping up with future financial trends, staying informed, monitoring your credit health and making proactive decisions, you can position yourself for financial success when the changes come.

-----------------------------------------------------------------------

Editor’s note: For more advice, call 502-624-5989 to make an appointment with an Army Community Service financial counselor in-person or request a virtual appointment.

Visit Fort Knox News at www.army.mil/knox for all Central Kentucky's latest military news and information.

Social Sharing