FORT CAMPBELL, Ky. – It’s never too soon to start putting money aside for retirement, but financial experts advise debt reduction before retirement planning will maximize retirement income.

A debt snowball method may help Soldiers and their Families make faster headway paying off debts so they can then invest larger amounts into retirement accounts.

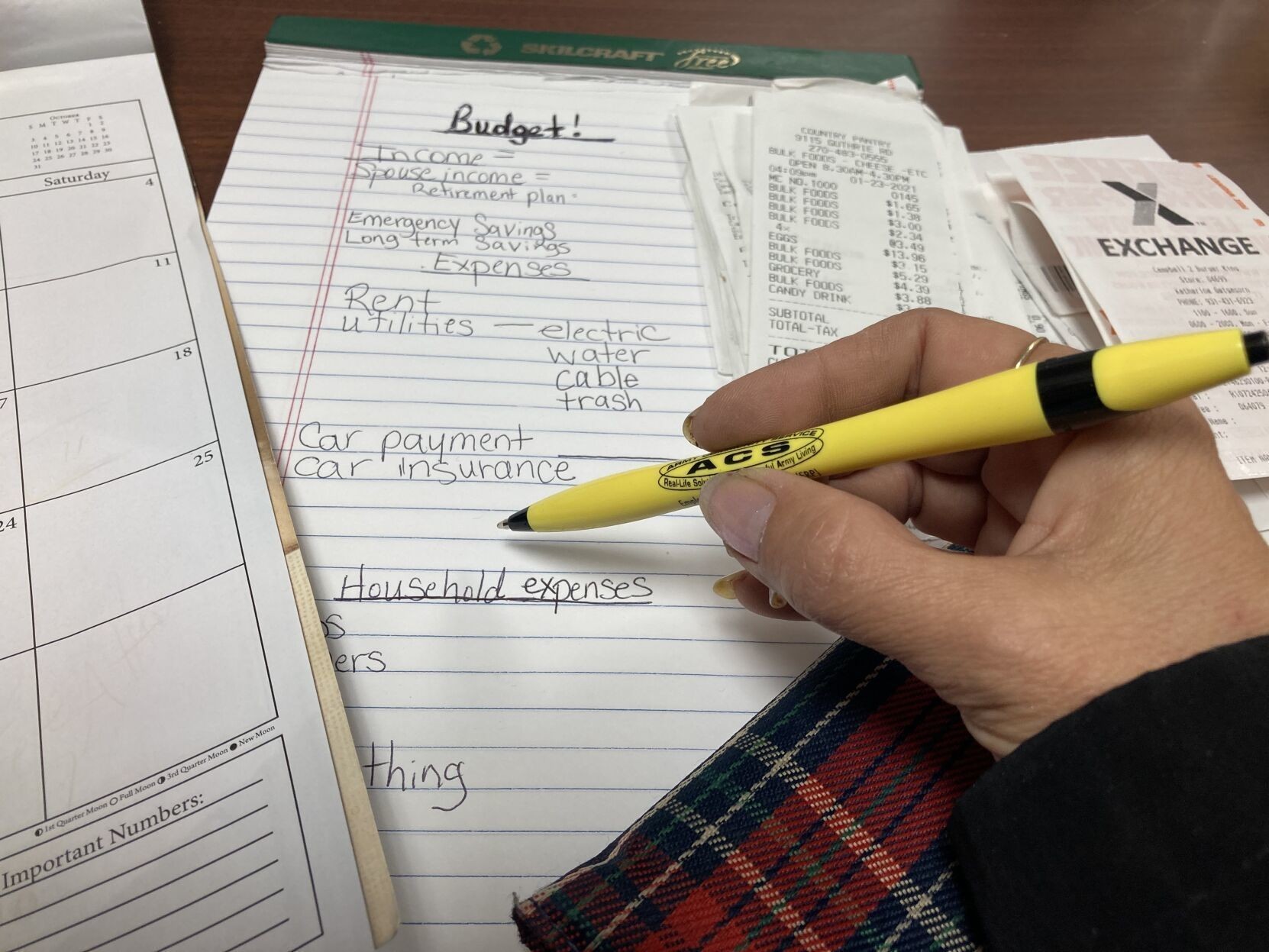

Soldiers and their Families can receive help developing a debt reduction plan and retirement plan from financial counselors at the Army Community Service-Financial Readiness Program.

Financial counselors at ACS-Financial Readiness are eager to help clients examine their budgets, analyze their spending and create realistic budgets that will allow them to use their money most efficiently.

Retirement planning

Terrence Jones, ACS-Financial Readiness program manager, said the debt snowball method is a debt-reduction strategy in which a person pays off debt in the order of smallest to largest, gaining momentum as debts are cleared. When the smallest debt is paid in full, the payment the person was making is rolled into the next smallest debt payment.

Tackling debt strategically – by either picking the largest debt, the smallest debt or the debt with the highest interest – can help consumers prioritize paying their debts down, Jones said.

The first step to planning for the future is to have a plan for debt payoff, he said. That may mean contributing less to retirement in the beginning but building that over time.

“Try to set your budget up where you can pay your debts, and if you want to save for retirement, do it at the same time, but don’t put so much in your retirement payments that it causes a problem,” Jones said. “Start with an amount that doesn’t cause a burden.”

As debts are paid, that allocated amount can be earmarked for savings or to pay on another debt.

“Try and work on getting your debt down, even if you have to start your retirement plan with the smallest amount, until your debts are paid,” he said.

After chipping away at those larger debts or higher interest debts, money should be set aside for emergencies, to avoid going into debt with credit cards or loans if something happens, Jones said.

“You want that emergency savings because you want something to fall back on,” he said.

Stagger payments

Financial counselors say it’s best to spread payments out so bills are not all due at the first, middle or end of the month.

“One thing Soldiers may have an issue with is [having all] payments due on the same date,” said Kevin Smith, personal financial readiness specialist, ACS-Financial Readiness. “If they can, talk to creditors to have their payments adjusted, so instead of having two payments due on the 15th of the month, they can have one changed to the first or the end of the month.”

Jones said counselors are available to help get their due dates changed in some cases.

“Look at the dates and determine what you can pay midmonth or what you can pay toward the end of the month,” he said. “We can help them set that up where it doesn’t create a burden.”

Counselors can help clients go through their budget, come up with a plan to pay debts and give them advice to stay on track with their finances and understand where their money goes, Jones said.

The key is not to ignore debts but to turn to ACS-Financial Readiness for counseling before finances cause trouble.

“Don’t let your pride get you to a place where you are afraid to say, ‘I need help,’” he said. “Don’t wait until they send you letters and it’s affecting your credit score and could affect your career with finan-cial issues.”

Finances also can cause rifts in Families when communication is lacking and action is not being taken. Ignoring financial problems does not make them disappear, Jones said.

“We have to talk about being responsible and accountable because you created these bills,” he said. “What we’re trying to do is remove stressors. You have to want help and we’re here to help. That’s why we have ACS-Financial Readiness.”

Although Army Emergency Relief is an option for Soldiers in some emergencies, having an emergency savings account is vital to avoid going further into debt, said Brett Ives, personal financial readiness specialist, ACS- Financial Readiness.

“Experts recommend you have three to six months of your living expenses in a savings account for emergencies, so you want to build that up at the same time you’re tackling debt through the debt snowball, and we can help with that plan,” Ives said.

Don’t ignore retirement match

Paying off debt is important, but so is making sure to put some money into retirement. Take ad-vantage of the matching funds that would go into a Thrift Savings Plan, so as not to lose out on employer contributions, Ives said.

“As long as it doesn’t cause hardship, it is something we want you to do,” he said. “It’s free money you’re turning down.”

To make an appointment with a financial specialist, call ACS- Financial Readiness at 270-798-5518.

Social Sharing